Need help and guidance?

We can’t provide guidance or advice about how to take your pension savings, but a specialist can.

Get help with finding guidance or advice, that’s right for you. Click on the guidance and advice menu item for more information.

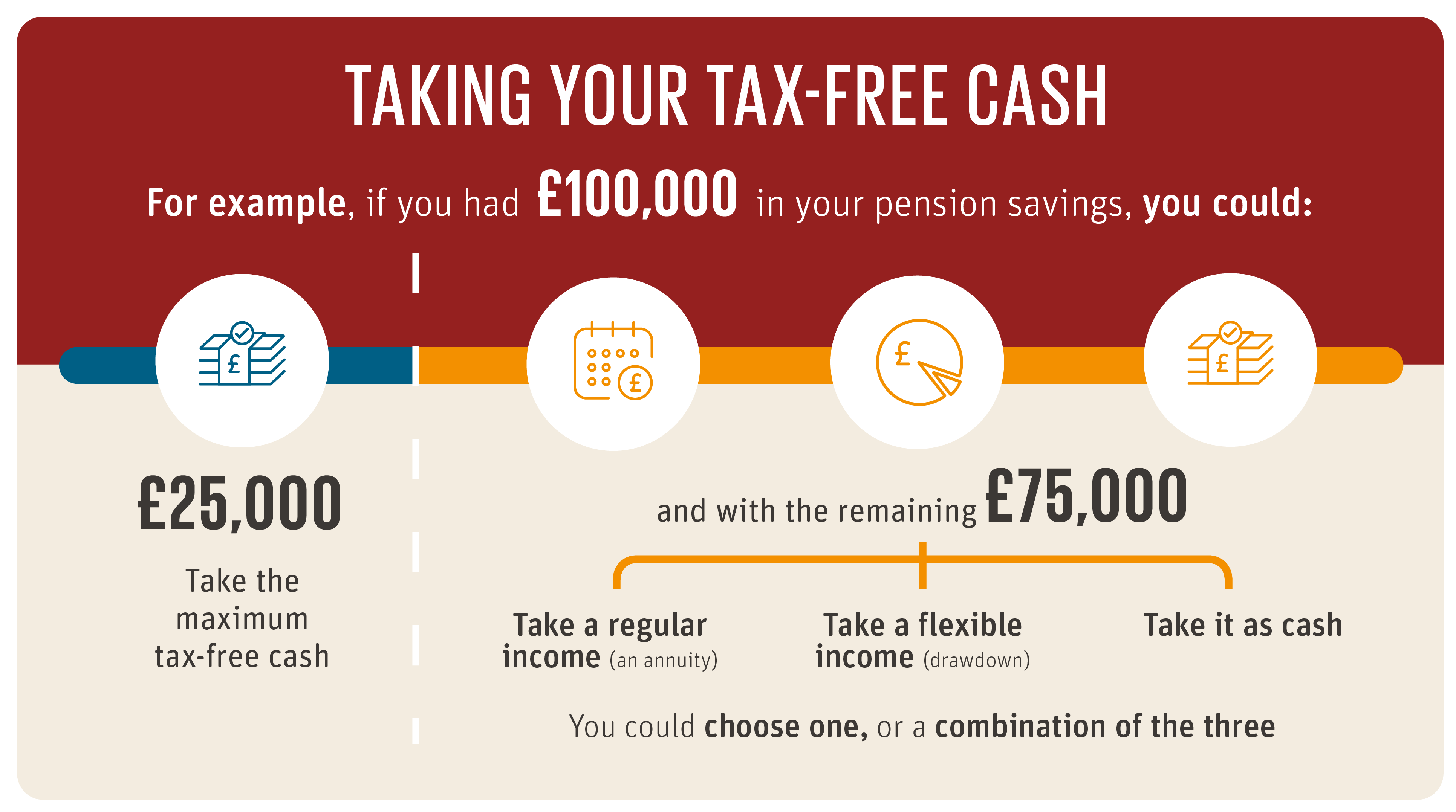

From age 55*, you can take up to 25% of your pension savings as tax-free cash if you want to. You can take the rest of your pension savings as one, or more, taxable cash lump sums.

Taking your savings as cash:

You can take some, or all, of your pension savings as cash. You can do that in a few different ways:

-

You can take 25% of your pension savings as a tax-free cash lump sum (although you don’t have to). If you want to access some, or all, of this tax-free cash, you’d need to set aside the other 75% and make a decision on how you’d like to use it. You could use it to buy a regular income (or annuity), or you could re-invest it and take money as and when you need it).

The maximum tax-free cash you can take from all your pensions is subject to the Lump Sum Allowance of £268,275. This allowance may be higher if you have previously applied for pension protection. -

You can also take some, or all, of your pension as lump sums and 25% of each lump sum is usually tax-free. The remaining 75% is subject to tax. If you only take part of your pension as a lump sum, the rest remains untouched and invested, and you can decide later how you would like to take it. If you chose this option, there are set annual allowances on how much you can still pay into your pension in the future without being charged tax. This is currently £10,000 each tax year (although the Government may change this in future). You will need to tell us each time you want to take a lump sum in this way.

The maximum tax-free cash is subject to the Lump Sum Allowance of £268,275. This allowance may be higher if you have previously applied for pension protection. -

If your pension savings are under £10,000 you may be able to take it all as cash, 25% of which is tax free. You may be able to take this kind of lump sum up to a maximum of three times from separate personal pension savings pots, but each lump sum must not exceed £10,000.

Things to think about

Generally, taking your pension savings as cash could be a good option for you if you’re looking to top up other pension income, or finance specific events or purchases in retirement. That could be anything from paying off a mortgage, to financing a wedding, to going on holiday.

Depending on how much you take as cash in one go, and how much other income you have coming in, the tax on it could be much higher than you are used to

Here are three things to ask yourself when you’re making your decision:

-

Will I have other income in retirement?

Taking your pension savings as cash may help with some short-term considerations, but it won’t provide an income in retirement. Do you have alternative income you’ll be relying on, either from work or other savings?

-

How long will my money last?

You may be thinking about taking your pension savings as cash and using that to fund some of your current needs. Make sure you’ve also got a plan in place for your longer-term income, and for looking after your family in the event of your death. You can get some additional guidance and advice if you need to.

-

Do I want to keep building up pension savings?

Remember: if you take your money as cash, from that point onwards, your annual allowance (the amount you can pay into a pension each year without a possible tax charge) will change. You’ll have a specific annual allowance in respect of your money purchase pension savings (the ‘money purchase’ annual allowance or MPAA), of £10,000 (unless you have already taken benefits through Capped Drawdown). You can find out more about tax and your pension here.

*the normal minimum pension age will increase to 57 from 6 April 2028 in line with changing legislation.